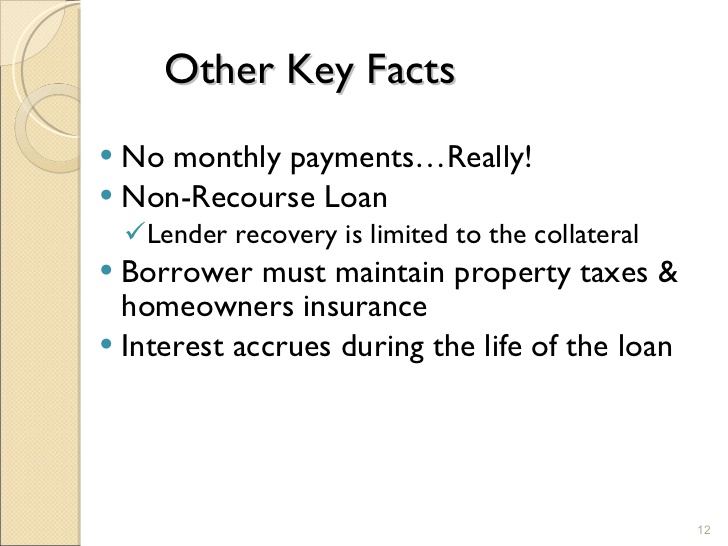

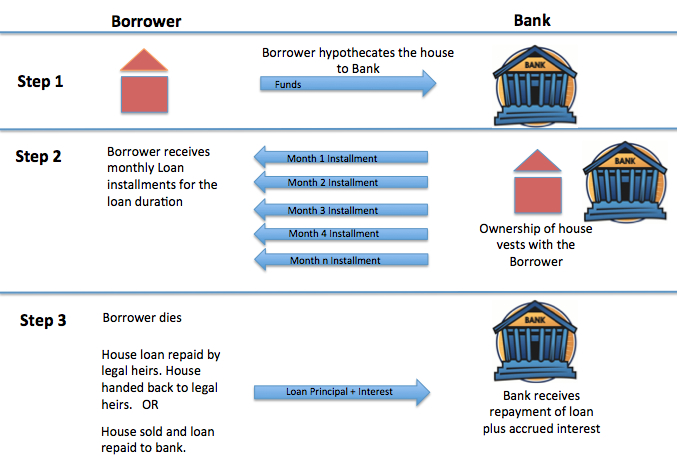

A reverse mortgage or home equity conversion mortgage (HECM) is a special type of home loan for older homeowners (62 years or older) that requires no monthly mortgage payments. Borrowers are still responsible for property taxes and homeowner's insurance. Equity is the current cash value of a home minus the current loan balance.

A reverse mortgage works much like a traditional mortgage, except in reverse. Instead of the homeowner paying the lender each month, the lender pays the homeowner. As long as the homeowner continues to live in the home, no repayment of principal, interest, or servicing fees are required. The funds received from a reverse mortgage may be used for anything, including housing expenses, taxes, insurance, fuel or maintenance costs.

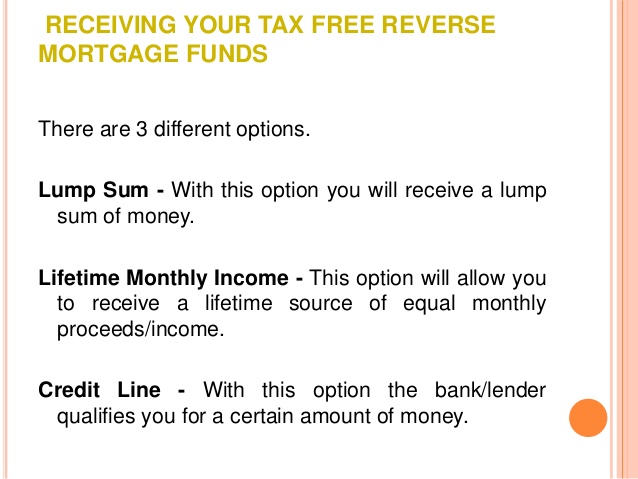

To qualify for a reverse mortgage, you must own your home. You may choose to receive the reverse mortgage funds in a lump sum, monthly advances, as a line-of-credit, or a combination of the three, depending on the reverse mortgage type and the lender. The amount of money you are eligible to borrow depends on your age, the amount of equity in your home, and the interest rate set by the lender.

Because the borrower retains ownership of the home with a reverse mortgage, the borrower also continues to be responsible for taxes, repairs and maintenance.

Depending on the plan selected, a reverse mortgage is due with interest either when the homeowner permanently moves, sells the home, dies, or the end of a pre-selected loan term is reached. If the homeowner dies, the lender does not take ownership of the home.

Instead, the heirs must pay off the loan, typically by refinancing the loan into a forward mortgage (if the heirs meet eligibility requirements) or by using the proceeds generated by the sale of the home.

End mortgage payments for life!

We've been helping customers afford the home of their dreams for many years and we love what we do.

Sterling Mortgage Services

CA BROKER NMLS

Company NMLS: 1460556 | CalBRE ID: 01376997

Licensed Only In: CA

www.nmlsconsumeraccess.org

Sterling Mortgage Services

Folsom, CA 95630

Phone: (855) 870-7334

info@sterlingmortgagehomeloans.com

![]() Powered By LenderHomePage.com

Powered By LenderHomePage.com